Audit Response Letter

Objective

Generate an automated template for an audit response letter, collect electronic signatures from signatories, and send the letter automatically via email.

The response letter can be generated either as a standalone document or as part of an audit workflow initiated by the company, if it is also a Looplex user. The response content is logged in the respective cases.

Our Client

This solution applies to all legal professionals who need to draft and send response letters to independent auditors regarding ongoing disputes where contingent liabilities have been identified and can be estimated and assessed.

The letter can be generated by in-house lawyers of a legal department using Looplex or by external attorneys representing a company or entity as their client.

Challenges

Companies are routinely audited for compliance validation and financial statement verification.

The “circularization letter” is a document through which the audit team contacts third parties who are external sources of information for updates or confirmation of accounting facts and their respective balances.

Lawyers representing the client in a dispute or supervising the case are the professionals responsible for addressing contingent liabilities that may result in provisions, providing risk or disbursement estimates when possible.

To fulfill this task, lawyers must receive requests, search their records for contingent liabilities, and draft a consistent response containing all necessary elements for the auditor, whether internal or external.

At the same time, lawyers have a legal duty to protect the confidentiality of their advice and attorney-client communications.

An audit procedure requiring clients to authorize their lawyers to respond comprehensively to inquiries and disclose confidential information risks undermining open communication between lawyer and client. This would discourage companies from discussing potential legal issues with their lawyers, fearing such discussions might become public and trigger liabilities that would not otherwise materialize.

A practical, automated solution is needed to balance these considerations while safeguarding the liability limitations of the signatories.

Solution

The template generates a general text capable of responding to standard audit circularization letter models sent to the client’s legal advisors, including those automatically generated by the Looplex platform.

1. Response Template

The document structure is based, with necessary adaptations for Brazil’s specific rules and peculiarities, on the Statement of Policy Regarding Lawyers’ Responses to Auditors’ Requests for Information by the American Bar Association (ABA).

To generate the letter, the template considers the following data from active cases managed in Looplex Cases:

- What are the objects of the disputes? (contingent liabilities in claims and related allegations)

- Is the risk for each object or claim remote, possible, or probable?

- Was the risk classification guided by the signatories’ expertise or judicial decisions on each claim?1

- What are the claim values (plaintiff demands)? Can the lawyers estimate a value with sufficient certainty at this point?2

2. Response Letter Content

The body of the document usually contains the following sections:

Client Authorization to Respond

Before responding to the auditor, the lawyer must have received explicit authorization from the client to share information regarding the cases under their care. If the client is organized as a “Group” in Looplex, the response may cover cases for all entities within the group. During setup, users must specify which entities are included in the response.

Limitation of Scope

The scope is limited to legal aspects of cases where the signatories have acted as lawyers in some capacity. If the signatories are not responsible or supervising the responsible parties, cases that should be answered by other lawyers should not be included.

Materially Relevant Items Only

Given Brazil’s mass litigation scale, the circularization letter may limit responses to disputes above a certain value. Users may also choose to group smaller cases into general blocks for explanation. Additionally, signatories note that only cases active as of the cutoff date (typically the end of the indicated accounting period) and containing materially relevant contingent liabilities are listed.

Contingent Liabilities and Undefined Contingencies

This section clarifies that only disputes with identified contingent liabilities (e.g., claims with defined monetary values) where clients are potential debtors, and where loss or disbursement risk can be estimated, are included.

In future updates, potential obligations from contracts or liabilities (e.g., guarantees or civil liability for damages) may also be included. Verify availability during generation and decide whether to add these disclosures.

To include potential gains (contingent assets), consider using another audit response letter template or adapting this document before sending it.

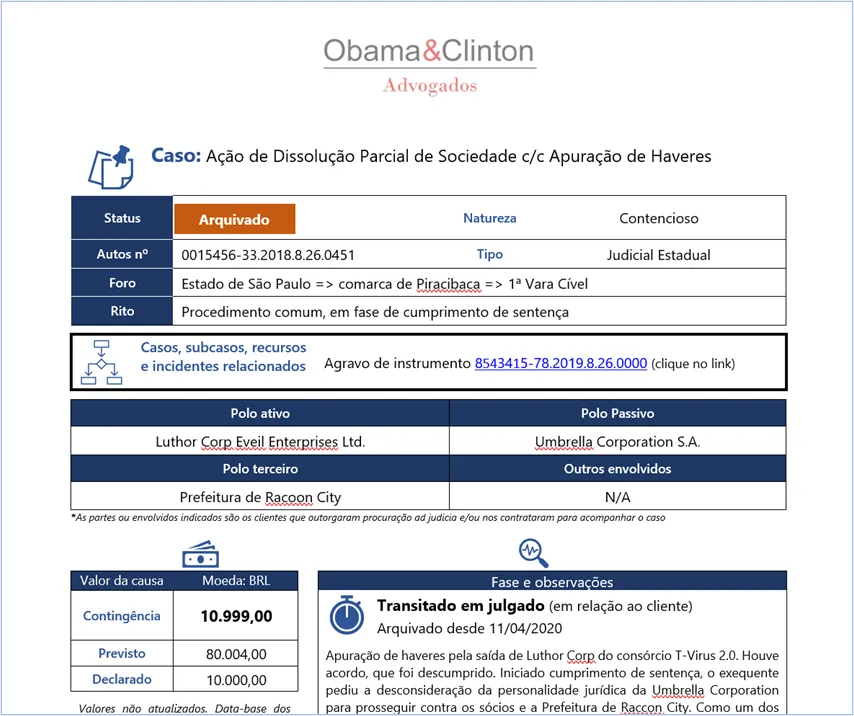

The system generates the selected elements, interpreting values in Looplex as:

- Expected Value – The estimated economic obligation in dispute, usually reflecting the maximum estimated value.

- Contingency Value – Estimated minimum expected value, often a percentage of the expected value based on applied risk assessment.

- Declared Value (or “Claim Value”) – Values assigned by the plaintiff in the dispute, which may not reflect the lawyers’ estimated expected value.

Limitation of Responses

The signatories list all relevant cases, subject to the document’s disclaimers. The system compiles a case list or states no cases fall within the request’s parameters. Case details are included as an appendix, essentially a filtered case report.

Outstanding Fees

The letter may address any unpaid fees related to the listed cases, whether the signatories are corporate legal department members or external counsel. This declaration is based on “to the best of our knowledge.”

Attorney-Client Privilege

A disclaimer ensures that no information beyond the auditor’s minimum requirements is disclosed, affirming that attorney-client privilege remains intact.

Limited Use of Response

This section reinforces that the response is limited to the auditor’s informational needs and restricts its use, especially if the recipient becomes or could become an adversary in litigation.

You can also customize the document style using your organization’s general settings for a personalized appearance:

3. Attachments to the Response Letter

The system generates and attaches case files for the selected entities. Attachments can be included in the letter document (Word) or exported as Excel reports using the reporting tool.

Different groups of cases can be handled separately—for instance, grouping smaller cases in an Excel sheet while highlighting significant cases in individual case files.

4. Associated Workflows

Once generated, the letter can be sent for digital signatures via connected systems (DocuSign, ClickSign, etc.). See integrations for more details.

Disclaimers

This response letter, like all Looplex-generated documents, is a reference template. Always apply your professional judgment and expertise to ensure consistency and accuracy.

Despite having versions in other languages (currently en-US), remember that the suggested template elements are tailored to Brazilian law and regulations. For example, obligations to report material violations that could result in contingent liabilities might be mandatory under U.S. law (e.g., Sarbanes-Oxley §307) but not under Brazilian law. Always exercise discretion in evaluating the generated document!